What is Allowable Remuneration to Partners in an LLP?

Introduction

Rewards and return to a Partner is the most crucial aspect for any partner. Whether the partner is investing in the LLP or serving with his skills to LLP, the return is sought. This aspect should not be neglected when you go for LLP Registration. Any income a Partner receives from an LLP is an important question and partners emphasise on receipt of maximum return from their investment made in the LLP. To incorporate the balanced remuneration clause in the LLP Agreement, the partners first need to know what the available returns are for their investments and efforts.

What a Partner can expect for his contribution in the LLP can be divided into following three heads:

- Remuneration

- Interest on Capital Introduced

- Share of Profit

Meaning

The phrase remuneration includes any salary, bonus, commission, or remuneration (by whatever name called) paid to a partner. The remuneration is normally payable to the partners who are actively contributing in the operations of the LLP. For rewarding their work and efforts alike any employee, the remuneration is payable to them.

Interest is paid to partners who have introduced the capital whether by way of cash or any other mode.

The phrase share of Profit assumes the percentage of profit distributed among the partners as return from the profit earned by the LLP with the capital introduced and efforts of the partners by the Partners in LLP. Share of Profit can be distributed among all the partners.

Here, there are some aspects explained with regard to the remuneration of Partners in LLP:

Which Partners are eligible for Remuneration from LLP?

The remuneration of partners of LLP is specifically regulated by and subject to the clauses of LLP Agreement. Whether Partner is Working or Non-working i.e. Sleeping Partner, the remuneration paid or payable shall be authorised by LLP Agreement.

However, a maximum limit is prescribed under –

Amount deductible under the Income Tax Act:

Remuneration to partners in an LLP:

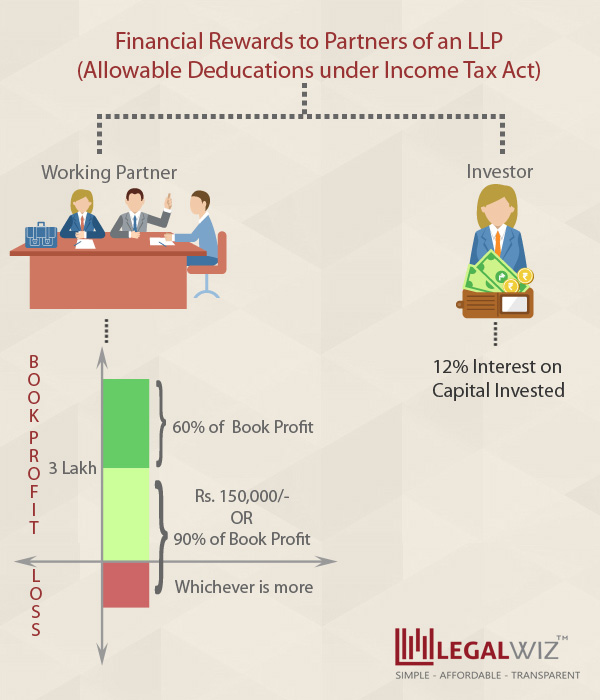

- Remuneration paid will be allowed as a deduction if it is paid to a working partner who is an individual.

- The remuneration paid to such working partner must be authorised by the LLP Agreement and the amount of remuneration must not exceed the limits given below:

If the LLP has paid remuneration more than limit prescribe above, the excess amount paid to partners is not allowable expense for deduction.

Interest on Capital Introduced:

The maximum interest allowed under Income Tax Act is simple interest at the rate 12% p.a. Any amount in excess of 12% is disallowed under the Act. The LLP Agreement shall authorise the payment of interest on the capital account. The percentage of interest payable may be incorporated in the LLP Agreement for authorising same.

Taxability in the hands of Partners:

Remuneration:

The remuneration received by the partners from LLP is taxable in the hands of Partners as Business Income. The income of remuneration is not included as share of profit.

Interest on Capital Introduced:

Interest paid on capital to partners is taxable in hands of Partners as Business Income.

Share of Profit:

The share of profit received by the partners, whether being working or Non-working Partner is exempted under Section 10(2A) of Income Tax Act.

Bottom Line:

Eligibility for returns and remuneration to partners in LLP depend on the designation of Partners or the terms entered into LLP Agreement filed during LLP Registrations and afterwards through changes. Hence, before proceeding to incorporate an LLP, the partners shall carefully decide about the designation and right of each partner in LLP.

It is also to be noted that although irrespective of the terms and limits of remuneration in LLP Agreement, the taxability of returns and remuneration of partners and profits of LLP is calculated as per Income Tax Act.

CS Prachi Prajapati

Company Secretary with a forte in content writing! Started as a trainee, she is now leading as a Content Writer and a Product Developer on technical hand of LegalWiz.in. The author finds her prospect to carve out a valuable position in Legal and Secretarial field.

Which ITR to be filed for such LLP Partners? For LLP’s income it is ITR-5, but for partners, which is the ITR?

Thanks!

Hello,

Partners of the LLP should file ITR in form ITR-2.

For more information, You can read our blog about “Quick Guide for Income Tax Return Filing”.

Or Get in touch with our team of CA/CS at support@legalwiz.in.