GSTR 3B : Return format

Introduction

Are you a business owner registered under the Goods and Services Tax (GST) in India? Then you know that filing your GSTR 3B return is an essential part of staying GST-compliant. But did you know that failing to file this document on time can result in some pretty hefty penalties? Yikes! Don’t let that happen to you. In this article, we’ll not only help you understand the ins and outs of the GSTR 3B return format but also emphasize the importance of timely compliance. So, get ready to dive into the exciting world of GST compliance and ensure that your business stays on the right side of the law.

GSTR 3B Return Format

GSTR 3B is a simple return form that businesses need to file online on the GST portal. Every GST-registered taxpayer needs to file GSTR-3B on the 20th of every month (or the 22nd/24th of every quarter if they are QRMP taxpayers). While figuring out how to file GSTR-3B, understanding its format is very important. At the beginning of the GSTR 3B form, you need to provide your GSTIN and legal name. After that, it contains 7 different tables, each of which require specific information to be filled in. The tables are as follows:

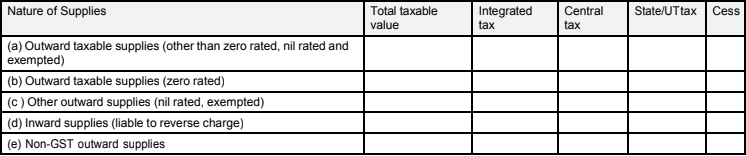

Table 1. Outward Supplies and Inward Supplies on Reverse Charge

This section is divided into four subsections:

- Firstly, Outward Taxable Supplies. In the subsection “Outward Taxable Supplies,” you should only include supplies on which you have charged GST. Accordingly calculate the value of taxable supplies by adding the value of invoices and debit notes, deducting the value of credit notes, adding the value of advances received for which you have not issued invoices, and deducting the value of advances adjusted against invoices.

- Secondly, Outward Taxable Supplies (Zero-Rated). This subsection includes only those supplies on which the GST rate is zero. Zero-rated supplies are exports or supplies made to SEZ.

- Thirdly, Other Outward Supplies (Nil Rated, Exempt). In the subsection “Other Outward Supplies (Nil Rated, Exempt),” include supplies that are exempt from GST or have a nil GST rate. Nil-rated supplies are those for which the GST rate is nil or have been exempt from GST.

- Fourthly, Inward Supplies (Liable to Reverse Charge). This subsection provides details of purchases made by unregistered dealers on which reverse charge applies.

- And finally, Non-GST Outward Supplies: This subsection contains details of any supplies made by you kept wholly out of GST. For example, alcohol and petroleum products.

In each of these subsections, you must provide the total taxable value and break this up into IGST, CGST, SGST/UTGST, and cess if any. You do not have to provide the GST rate, only the total tax values.

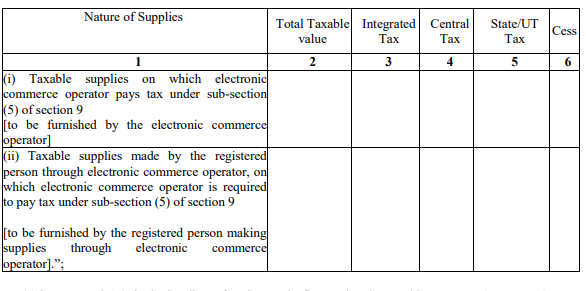

Table 2: Details of E-commerce Supplies

This section was added as a part of the modification to GSTR-3B vide the CGST Notification 14/2022 dated 5th July 2022. In this section, e-commerce operators must fill in Clause (i) with sale value and taxes payable, whereas e-commerce sellers should fill Clause (ii). It is important to enter details of only the sales carried out through the e-commerce websites. This section must not contain any information already mentioned within Table 1.

Table 3: Inter-State Supplies Made to Unregistered Persons, Composition Taxable Persons, and UIN Holders

This section is further divided into two sub-sections:

- Outward Taxable Supplies: You must mention the inter-state supplies you make to unregistered persons, composition dealers, and those holding a UIN.

- Inward Supplies on which Tax is to be paid on Reverse Charge Basis: You must mention the inward supplies you receive from a registered person, on which you are required to pay tax under the reverse charge mechanism.

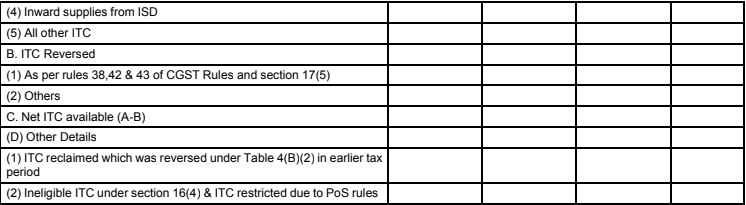

Table 4: Eligible ITC.

Section 3.4 of GSTR-3B pertains to the input tax credit (ITC) that businesses can claim for taxes paid on their purchases, which they can use to offset their GST liabilities. It is important to report these details accurately to avoid any errors or penalties.

The section is divided into three parts, which are as follows:

(A) ITC Available:

This section requires businesses to report the total value of ITC available for each type of tax, such as IGST, CGST, SGST, UTGST, and Cess. The available ITC should be reported separately for the following categories:

- Import of goods

- Import of services

- Inward supplies on reverse charge (excluding those reported under import of goods and services)

- Inward supplies from Input Service Distributors (ISD)

- All other ITC

Note that businesses do not need to report input tax credit on closing stock in this section, as it must be reported through the TRAN-1 and TRAN-2 forms.

(B) ITC Reversed:

This section requires businesses to report the value of ITC that must be reversed for various reasons, such as when input goods or services are used for both business and personal purposes. The following types of ITC must be reported separately:

- Reversal of ITC as per CGST Rules 38, 42, and 43, and section 17(5) of the CGST Act

- Reversal of ITC on inputs, input services, and capital goods used for taxable, exempt, and nil-rated supplies

- Ineligible ITC under section 17(5)

- Any other ITC that has been reversed by the business

(C) Net ITC Available:

This section calculates the net ITC available to the business by subtracting the value of ITC reversed (as reported in section 3.4(B)) from the ITC available (as reported in section 3.4(A)).

(D) Other Details:

Businesses must report any other relevant details, including the value of Input Tax Credit (ITC) reclaimed that they reversed in the previous tax period, and the value of ITC that they restricted due to the place of supply provisions. They are required to report this information in this section.

Table 5 Tax Liability

This section requires you to report your tax liability on outward supplies made during the tax period. It includes the tax payable on supplies made to registered taxpayers as well as those made to unregistered taxpayers. You need to break down the tax liability into the following components:

- IGST – Tax payable on interstate supplies

- CGST – Tax payable on intrastate supplies within the same state

- SGST/UTGST – Tax payable on intrastate supplies within the same state for states that are not union territories

- Cess – Tax payable on goods and services that are subject to cess

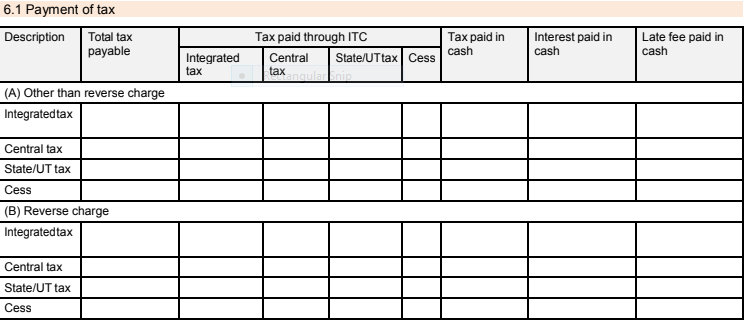

Table 6 Payment of Tax

In this section, you need to mention the total amount of tax that you are liable to pay. You also need to mention the amount of tax that you have already paid through cash or ITC. If you have not paid the full amount of tax due, you need to make the payment before the due date to avoid penalties.

Table 7 TDS and TCS Credit

This section applies only to those taxpayers who are required to deduct or collect tax at source. If you are such a taxpayer, you need to report the total amount of tax that you have deducted or collected during the tax period. You also need to mention the amount of tax that has been credited to your electronic cash ledger.

New Changes in GSTR-3B

As we step into the new fiscal year, the Union Budget 2023 has brought in some significant changes in the GST laws in India. One of the crucial updates is the revision in the GSTR-3B format, Here’s everything you need to know about the latest changes in the GSTR-3B form format and other updates.

- Firstly, there has been an introduction of new fields for HSN codes of goods and services and the reporting of ITC on the import of goods. Taxpayers can now download the GSTR-3B form from the GST portal in the new format.

- Moreover, the Union budget 2023 has brought in important GST updates. Such as the amendment of Section 16 of the GST Act. As per the amendment, buyers who fail to pay their supplier the invoice value, including the GST amount, within 180 days from the date of issue of the invoice, must pay an amount equal to the ITC claimed along with interest under Section 50.

- Another amendment that taxpayers should take note of is the revision of Section 17(5). As per the revised section, taxpayers cannot claim input tax credit on CSR expenses.

- Finally, the Union Budget 2023 has also amended Section 10 of the CGST Act, allowing businesses that supply goods through an e-commerce operator to opt into the composition scheme.

Conclusion

GSTR 3B return form is an important document that businesses registered under GST in India need to file on a monthly basis. It contains critical information such as details of outward supplies, input tax credit, tax payable and paid, and other necessary details. Hence, it is very important to file in a proper and timely manner. We hope this article will help you file this essential component of your compliance calendar for 2023 without any hassle.

Frequently Asked Questions

Monjima Ghosh

Monjima is a lawyer and a professional content writer at LegalWiz.in. She has a keen interest in Legal technology & Legal design, and believes that content makes the world go round.